What’s Wrong with Impact Investing — and How AI Can Make It Right

At the end of this century, we’ll look back and credit impact investing with revolutionizing modern capitalism. That may sound naïve given the recent backlash against sustainability and ESG (environmental, social, and governance), but I didn’t arrive at this view lightly.

I’m an unlikely advocate for impact investing. I began my career at GE, a company that prided itself on maximizing shareholder returns under Jack Welch. I then spent a few years at a private equity firm known for slashing expenses. I concluded my career at McKinsey & Company, which, of late, hasn’t exactly been a beacon of corporate responsibility.

Along the way, I earned an M.B.A. from the University of Chicago, where Milton Friedman published his article, “A Friedman doctrine‐- The Social Responsibility of Business Is to Increase Its Profits.” Even though I (mostly) retired in my mid-40s, I still help business owners and managers wring money out of companies. Capitalism is a game I enjoy playing.

How did I end up on the same side of the table as those who believe unfettered capitalism is destroying society? It’s because they offer an alternative that might work.

Robinhood Capitalism

The goal of capitalism is simple — maximize the size of the pie. It’s easier to give everybody what they need and want in a land of abundance.

The problem is that economic output doesn’t guarantee happiness. That’s the sentiment expressed in one of my favorite quotes, extracted from a speech by Robert F. Kennedy at the University of Kansas in 1968.

Yet the gross national product does not allow for the health of our children, the quality of their education or the joy of their play. It does not include the beauty of our poetry or the strength of our marriages, the intelligence of our public debate or the integrity of our public officials. It measures neither our wit nor our courage, neither our wisdom nor our learning, neither our compassion nor our devotion to our country, it measures everything in short, except that which makes life worthwhile. And it can tell us everything about America except why we are proud that we are Americans. — Robert F. Kennedy

We want to live in safe and supportive communities. We want access to fresh air, clean water, nutritious food, and healthcare. We want our family and friends to be treated with respect and dignity.

This is where capitalism's ideals run headlong into life’s realities. A massive GDP creates the conditions for success, but too often, the system falls apart as we convert economic output into quality of life.

We incentivize the private sector to maximize profits and wages, only to tax those profits and wages to fund governments and non-profits. We then ask those entities to fix problems caused by the private sector and produce goods and services that aren’t economically viable.

I call our existing system “Robinhood Capitalism” because it takes from the resource-rich and gives to the resource-poor, tasking the resource-poor with solving problems ignored or created by the resource-rich. There’s plenty to criticize about the public and social sectors, but we don’t exactly set them up for success.

Impact investing offers an alternative. The private sector is best positioned to minimize externalities and efficiently produce public goods and services. Why don't we incentivize it more directly?

Money Talks

Milton Friedman’s 1970 doctrine is often summarized as “the business of business is business.” His core argument is that executives are agents of the individuals who own the corporations. Individuals have responsibilities, but corporations don’t.

In either case, the key point is that, in his capacity as a corporate executive, the manager is the agent of the individuals who own the corporation or establish the eleemosynary institution, and his primary responsibility is to them. — Milton Friedman

Friedman conveniently ignores that shareholders have objectives beyond maximizing profits. Like many people, I own Apple stock through passive index funds. I care about the environment, social mobility, and human rights. How are my priorities communicated to executives?

They’re not.

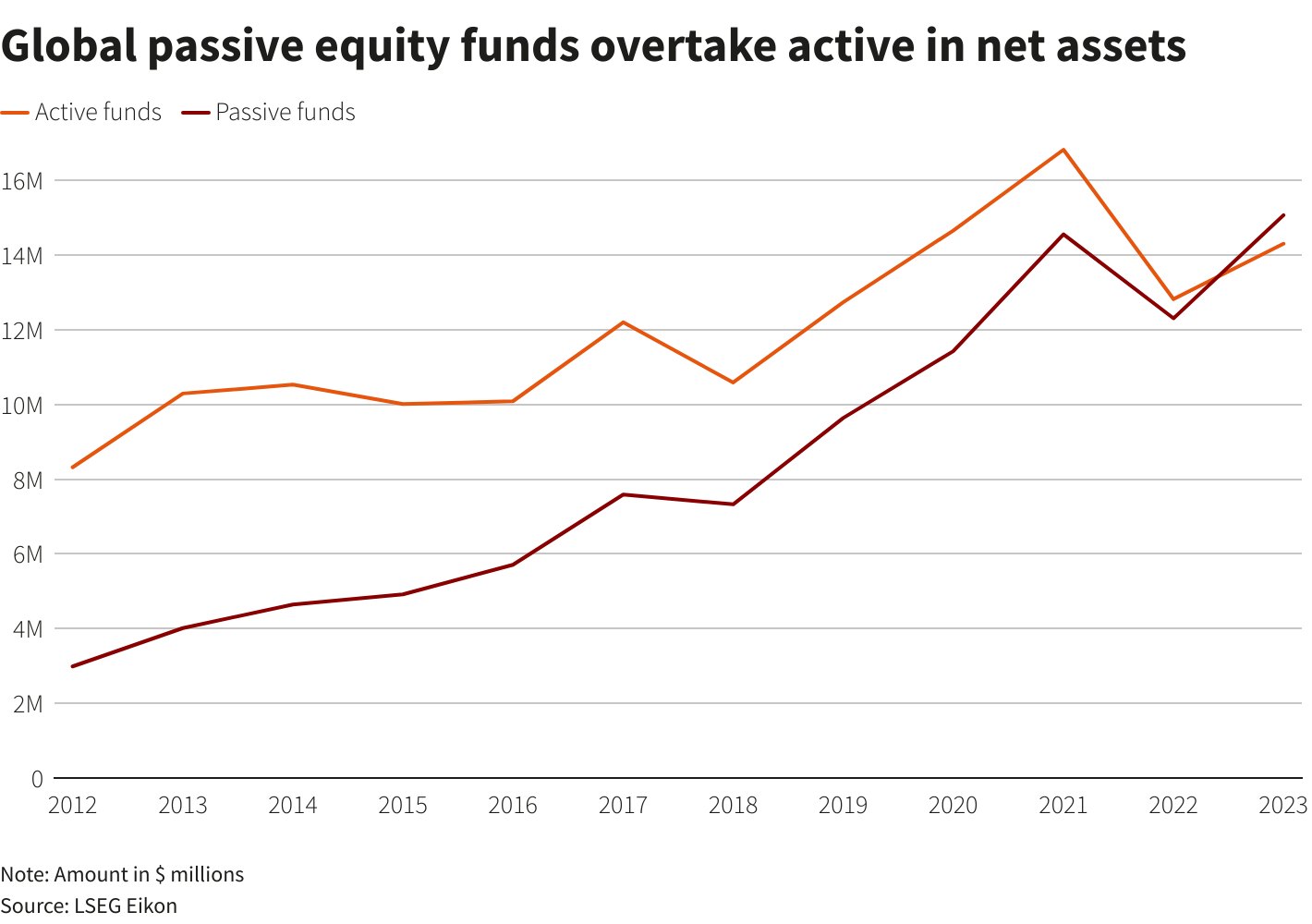

Asset managers responsible for passive index funds allocate capital based on market capitalization. The more valuable a company becomes, the more capital it receives. My money talks with the voice of my asset manager, not mine.

This isn’t a criticism of passive index funds. For most people, they’re the ideal vehicle for long-term wealth creation. Diversification and low fees are free lunches, and most active managers don’t beat the market. As a result, investors have more than $15 trillion stashed away in passive equity funds.

SOURCE: Reuters

My criticism lies with the alternatives. What if I want my money to deliver financial returns and social benefits? There’s no shortage of enthusiasm or capital for impact investing — but the industry is broken. The problem isn’t passion; it’s flawed strategies and outdated operating models.

Doing Fine

The promise of impact investing is “Doing Well by Doing Good” — investors can profit and make the world a better place. It’s a fantastic marketing slogan, but does it stand up to scrutiny?

Let’s begin with “doing good,” where results are mixed. On one hand, corporate disclosures have increased significantly. You can find structured, audited data for several metrics like GHG (greenhouse gas) emissions, which hasn’t always been true.

Many organizations have also named sustainability leaders responsible for reporting, third-party disclosures (e.g., Climate Disclosure Project), and engaging with external stakeholders. For example, Lisa Jackson reports directly to Apple’s CEO, Tim Cook, and leads the 2030 environmental initiative.

On the other hand, the industry can’t even agree on a framework. There’s the GRI, TCFD, ISSB, CSRD, CMP, SDG, PRI, and let’s not forget the CDP. I made one of those up. Do you know which one? Do you care?

Then there’s the lonely sustainability leader. I was a partner at McKinsey & Company for years. Do you know how often the sustainability leader was consulted on a major strategic or operational decision during one of my projects? Never — not once. The CEO, CFO, COO, CIO/CTO, and occasionally the CHRO had seats at the table. The sustainability leader wasn’t even in the same room.

My critique is harsh, but I’m generally optimistic. Companies and markets don’t change overnight. These are positive signs, and I can make a strong case for the “doing good” part of the promise; “doing well” is another story.

The Conscience Tax

When I first learned about impact investing, “doing well” meant beating the market. The hope was that sustainable companies would outperform profit-maximizing companies over the long term. That turned out to be wishful thinking.

In 2019, Royal Bank of Canada (RBC) examined dozens of academic studies on the financial returns of impact investing. A few researchers found evidence of outperformance (e.g., during a crisis), but the overwhelming majority found no significant performance differences.

To me, this was encouraging news. Responsible companies don’t sacrifice financial returns for doing good, so impact investing is viable even for people who value financial returns above all else.

That is, until you read the fine print. Most of the studies looked at risk-adjusted returns. They also didn’t account for fees charged by the asset managers. This is where the fairytale falls apart.

I researched four mutual funds offered by asset managers specializing in impact investing. Here they are in decreasing order of portfolio size:

Parnassus Core Equity Fund — Investor Shares (PRBLX)

Nuveen Large Cap Responsible Equity Fund A Class (TICRX)

Calvert US Large Cap Core Responsible Index Fund Class A (CSXAX)

Domini Impact Equity Fund Investor Shares (DSEFX)

The first shortcoming of these funds is that they don’t track the overall market. Betas range from 0.93 to 1.05. The tracking errors make sense when you look at the strategies. Here’s an example from the Nuveen Large Cap Responsible Equity Fund A Class disclosure:

It will not generally invest in companies significantly involved in certain business activities, including but not limited to the production of alcohol, tobacco, military weapons, firearms, nuclear power, thermal coal, and gambling products and services.

Screening methods like this introduce tracking errors. It’s also profoundly misguided. If you care about climate change, wouldn't you want to own companies involved in nuclear power? Or, to be more provocative, if you care about gun safety, wouldn't you want to reward firearm manufacturers doing the most to make their products safe?

Exclusionary screening is a simplistic strategy that destroys what Harry Markowitz called “the only free lunch in investing“ — diversification.

There’s a debate to be had over investment strategies. I believe impact investing should reward current contributions rather than penalize past decisions. Do you care more about ExxonMobil’s decision to enter the fossil fuel industry in 1866 or what it’s doing to transition to clean energy today? I care more about the latter.

That said, there’s a bigger elephant in the room than tracking errors and investment strategies — fees. Impact investing asset managers charge for all of their work screening companies. Net expense ratios range from 0.46% to nearly a whole percentage point.

SOURCE: Mutual fund prospectuses

The two funds with somewhat competitive net expense ratios, TICRX and CSXAX, also charge loads of 5.75% and 4.75%, respectively. To put that into perspective, the leading passive index mutual fund from Vanguard (VFIAX) has a net expense ratio of 0.04% and no load.

Doing good comes at a hefty price. By definition, impact investing is an active trading strategy. That means active trading fees minus the hope of market-beating performance (alpha) — a terrible deal for investors.

However, the current criticism of impact investing is misplaced. Research proves there’s no “tax” on companies pursuing social impact. Companies can do well and do good. People who claim sophisticated companies can’t walk and chew bubblegum ignore the facts.

For investors, it’s a different story. There’s a tax for doing good — high fees. Somebody has to pay all those researchers who gather impact data, screen companies, construct portfolios, and write impact reports. That’s why I don’t invest in impact funds — they’re too expensive.

Efficient Intelligence

Traditional equity funds have two metrics to balance — risk and return. For impact funds, the world is more complicated.

First, investors don’t share a common definition of “doing good.” An 8% financial return is the same whether you measure it in dollars or yen. An 8% reduction in greenhouse gas emissions isn’t the same as an 8% increase in diversity.

Second, the data is a mess. Regulatory agencies ensure financial data is mostly standardized. There’s room for interpretation in Generally Accepted Accounting Principles (GAAP), but at least there’s a standard. The impact investing industry seems to create new “standards” every year.

Third, valuing contributions involves more nuance. How do you decide whether Apple has done more than Microsoft on human rights? What about Apple compared to a smaller company with fewer resources like Juniper Networks (JNPR)?

Finally, impact funds must report on both financial and non-financial returns. Investors want to know how their money contributes to a better world. That’s the entire value proposition of the product.

This adds up to outrageous expense ratios. For impact investing to succeed long-term, it must solve its cost problem.

Fortunately, AI offers hope. Digital workers can dig through unstructured data, build portfolios, and generate impact reports at a fraction of the cost of human workers. AI also offers something the industry has never truly delivered — personalization.

I shouldn’t have to comb through dozens of prospectuses to find a fund that aligns with my impact priorities. Instead, I should be able to tell an asset manager what I care about, and they should invest my money accordingly. That’s what I mean by personalization.

AI has the potential to reshape how we invest. Imagine being able to buy a diversified portfolio of companies pursuing impact priorities you care about for an expense ratio competitive with passive index funds. That would finally elevate “doing well by doing good” from a catchy slogan to a kept promise.

v1.0

I like to write, but I also enjoy programming. Last year, I created an AI platform that turns research papers into short podcast episodes. It was a fun way to experiment with the latest AI models and keep up with the torrent of academic research. This year, I tried something more ambitious.

Rather than wait for someone else to build what I’m describing, I did it myself. You can find the project at purposefund.com. Anyone can create an account and use the site for free.

Purposefund is a minimum viable product built with my mediocre design and programming skills. That said, it does what I need from version 1.0. Here’s how it works:

You indicate what you care about by allocating 100 points across impact priorities, such as emissions and social mobility. There are six priorities to start, but the platform is scalable to any number over time.

AI scours the web to find contributions toward your priorities from each S&P 500 company, documenting each action and source. AI then writes positive and negative critiques of each company’s contributions.

AI force ranks each S&P 500 company against others in its sector. The AI considers multiple factors, including the magnitude of the impact and the specificity of the disclosures.

You receive an instant, personalized portfolio of companies doing the most to advance your impact priorities on an absolute (highest overall) and relative (highest vs. peers) basis.

You can explore what each company is doing by diving into the action reports, including each company’s weighted sector rank based on your unique priorities.

Once you have your portfolio, you can adjust the investment amount, portfolio size, and whether you want absolute or relative rankings. Each portfolio has the same sector weights as the S&P 500 to promote diversification, even for smaller portfolios. When you’re ready, you can download your portfolio as a spreadsheet.

Each time the site updates, AI generates about 3,000 action reports (500 companies x 6 impact priorities). Preparing each impact report would take a human worker about one hour. I don’t have a scientific way of estimating the time it would take for humans to rank the companies (11 sectors x 6 impact priorities), but it’s probably 5–10 hours per ranking to do well.

I plan to update the actions monthly so the reports are always current. The rankings can be done less frequently since passive index funds typically rebalance quarterly. If I could find people to do this work for $15 an hour, it would cost $570,000 annually.

What’s the cost for AI to do the same work? About $1,500 annually. That’s what I’d pay in fees to a traditional impact fund to manage $150,000, and they don’t even provide the same level of personalization and in-depth reporting as Purposefund.

I realize there’s more to managing a fund than determining how much money to invest in each company. However, Vanguard does the other work for 0.04% per year. Even allocating 0.20% to admin expenses, a small AI-powered impact fund should have a net expense ratio below 0.25%.

I have a long backlog of features I want to build. For example, I’d like a “news feed” of my portfolio’s contributions since my last visit. Eventually, I’d love a “trade now” button that integrates with an online brokerage platform, so I don’t need to enter 50 orders manually.

I didn’t build Purposefund to make money. I built it to prove a point. If I can do this with some rudimentary programming skills and a couple of grand, we should expect more from established asset managers. I’ll be excited if a firm with more experience and resources builds a better mousetrap than me sitting at my kitchen table with a laptop.

For now, I’ll keep adding features to Purposefund. I created a Patreon site for those who want to support future development. Please send me your ideas and suggestions. I can’t promise to deliver them all (mainly due to my lack of skills), but I’ll do my best to upgrade the site over time.

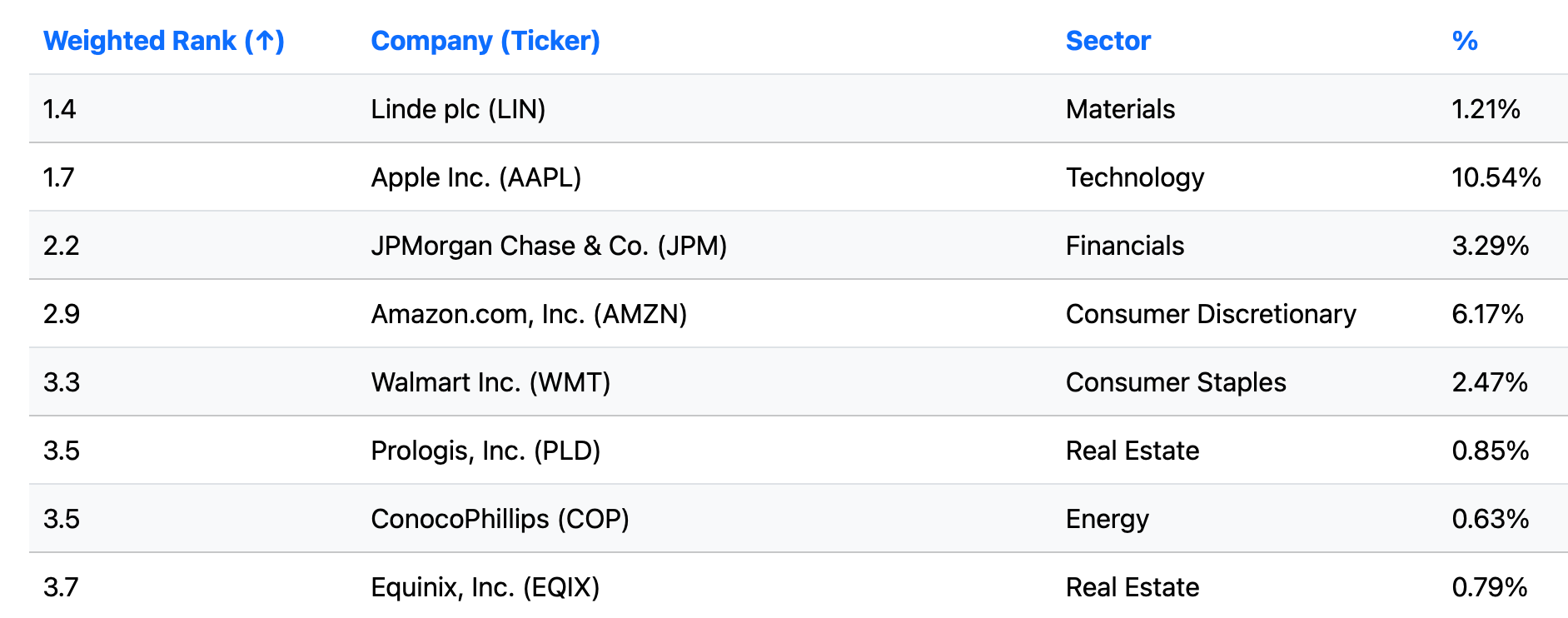

Snapshot of my Purposefund portfolio

My goal is to reduce the incremental cost of impact investing to zero. It’s absurd to choose between expensive impact funds and soulless passive index funds. I want my money to speak for me, and AI provides a path to making that happen.

Disclaimer: The content of this article is provided for general informational purposes only and does not constitute investment advice, financial planning, or a recommendation to engage in any specific investment strategy. Readers are encouraged to consult a qualified financial advisor before making investment decisions.